Financing a fleet is not one decision. It is a stack of decisions about what to fund, when to fund it, and how much control you are willing to trade for the capital. Most first-time operators overestimate the check they need to start, because they assume they have to pay for the software, the payments infrastructure, the support desk, and the vehicles all at once, upfront. You do not. This lesson walks through every realistic way to fund a shared-mobility fleet, the honest pros and cons of each, and how a revenue-share operating model changes the size of the check you actually write.

Operator education, not professional advice

This lesson is educational only. It is not tax, legal, accounting, or financial advice. Loan programs, Section 179 and other tax treatment, interest rates, and every financing term below vary by lender, by your borrower profile and credit history, and by jurisdiction, and they change over time. Treat any figure here as a starting point to model, not a quote. Confirm anything specific with a qualified accountant, attorney, or lender, and check current rules with the relevant authorities before you act.

Start with what you are actually financing

Before you compare loans and investors, split your costs into three buckets. Financing the wrong bucket with the wrong instrument is how operators end up over-leveraged or over-diluted.

- Hardware. The connected vehicles and their IoT modules. This is the only genuinely capital-intensive bucket. Levy is hardware-agnostic across 30+ IoT vendors and keeps a catalog of 150+ fleet-ready electric vehicles, but you still buy the vehicles. Levy sources, integrates, and retrofits third-party hardware. It does not manufacture it, and it is not a lender.

- The operating stack. Rider apps, operator dashboard, payments, identity and fraud checks, disputes, collections, support. Traditionally you build or license all of this and staff it. This is where most first-timers massively overestimate the upfront number.

- Working capital. Charging or battery swapping, repairs and spare parts, rebalancing labor, marketing, and the cushion to survive the first few months while utilization ramps.

The cheapest capital is the capital you never raise

Every dollar of the operating stack you convert from an upfront purchase into a pay-as-you-earn cost is a dollar you do not have to borrow or give away equity for.

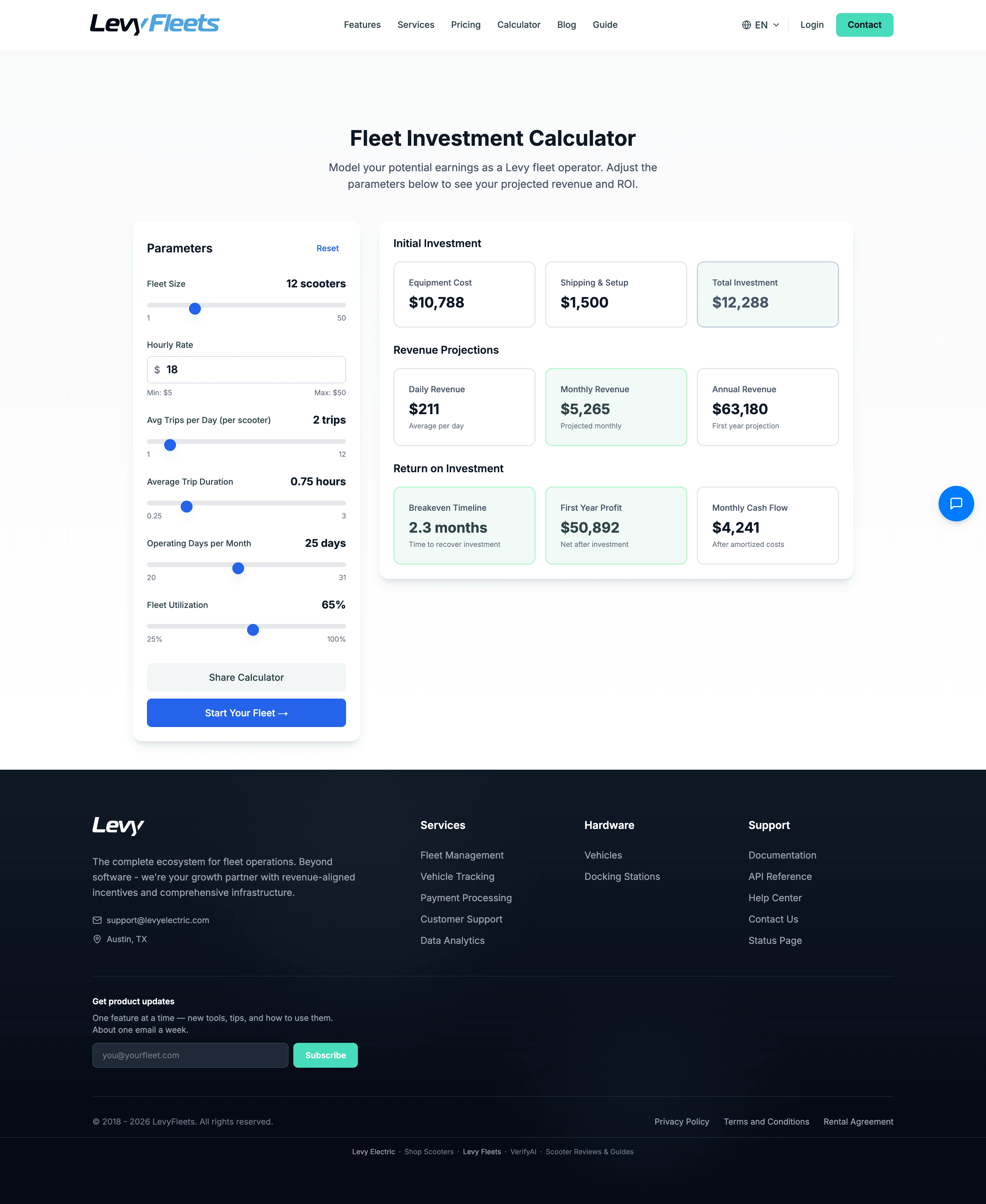

Model the target before you shop for money. Run your city, fleet size, and pricing through the Fleet Estimator, then read the full scooter rental business profitability breakdown for the assumptions behind it. Your breakeven ride count tells you how much runway each option has to buy.

Option 1: Self-funding

Self-funding means you cover the fleet from your own cash, savings, or reinvested earnings from a related business. It is how most single-city fleets start.

How it works: you buy a small batch of vehicles, get them earning, and recycle the revenue into the next batch. No lender, no investor, no paperwork.

Pros:

- Full ownership and full upside. You keep 100 percent of the profit and every decision.

- No interest, no dilution, no underwriting, no personal guarantee.

- Fastest possible start. You are live as soon as hardware arrives.

Cons:

- Growth is capped at your own bank balance. Scaling is slow and lumpy.

- It concentrates personal risk. One bad season or theft cluster can wipe out the buffer.

- Opportunity cost. Capital tied up in vehicles is doing nothing else.

Best for: a pilot you can fund out of pocket and grow from cash flow. Watch out for: spending your whole balance on hardware and leaving nothing for the ramp.

Option 2: Bank loans and SBA loans

Debt lets you buy more vehicles than your cash allows while keeping all of your equity. In the United States, the most common paths are a conventional bank term loan or line of credit, and loans backed by the Small Business Administration (SBA).

How it works: the SBA does not lend directly. It guarantees a portion of a bank loan, which lowers the lender's risk and gets you better terms than you would get unsecured.

- SBA 7(a): the general-purpose program, loan amounts up to 5 million dollars, usable for equipment and working capital.

- SBA 504: structured for fixed assets. Better fit if you are also financing a facility or heavy equipment.

- SBA microloans: up to 50,000 dollars, a realistic first rung for a small pilot fleet.

Those program ceilings are set by the SBA, but the amount, rate, term, and whether you qualify at all depend on the individual lender, your borrower profile and credit history, and current program rules, which change over time. Confirm the specifics with a lender before you plan around them.

Pros:

- The lowest cost of capital among debt options, especially the SBA-backed programs.

- You keep all of your equity and build business credit for the next round.

- Fixed, predictable repayment you can plan around.

Cons:

- Almost always requires a personal guarantee and often collateral.

- Slow underwriting (weeks to months) that usually wants a track record, commonly around 2 years.

- Repayment is rigid. You owe the same amount in peak season or a dead January.

Best for: operators with some history who want to scale without giving up equity. Watch out for: taking on fixed debt before utilization is proven, which forces loan payments out of a fleet that has not found its market.

Option 3: Equipment leasing and financing

Equipment financing is debt where the vehicles themselves are the collateral. Because the asset secures the loan, it is often easier to qualify for than a general business loan, even without a long history.

How it works: a leasing company or equipment lender pays for the hardware, and you repay over a term that ideally matches the vehicle's serviceable life. A lease may end with a buyout option or a return; a finance agreement usually ends with you owning the asset.

Pros:

- Preserves cash. You spread hardware cost over the months the vehicles are earning, not on day one.

- More accessible than unsecured debt because the equipment backs the deal.

- Predictable payments, plus potential tax treatment (for example Section 179 expensing, which your accountant should confirm).

Cons:

- You pay interest and fees, so total cost is higher than paying cash.

- Depreciation risk. Micromobility hardware evolves fast and can wear out before a long lease ends.

- With a true lease, you may own nothing at the end.

Match the term to the vehicle, not the balance sheet

A lease that outlives the hardware is a trap. Because Levy sources hardware and stocks common OKAI, Segway, and similar spare parts in the US so parts ship in days rather than weeks, you can keep vehicles serviceable longer and align the lease term to a realistic useful life instead of guessing.

Best for: operators who want to scale the fleet size without draining cash, and who are comfortable with asset-backed debt. Watch out for: financing fast-moving hardware on a term longer than it will realistically last.

Option 4: Revenue-based financing

Revenue-based financing (RBF) advances you capital that you repay as a fixed percentage of your monthly revenue until you hit an agreed cap. That cap commonly falls in the range of 1.3x to 1.5x of the amount advanced, but it varies by provider and by your revenue profile, so treat that range as a planning estimate and read the actual term sheet.

How it works: instead of a fixed monthly payment, you remit a slice of revenue. In a strong month you pay back faster; in a slow month you pay less. No equity is given up, and often no personal guarantee.

Pros:

- No dilution and no board seat. You keep control.

- Payments flex with actual revenue, which protects cash flow in a slow stretch.

- Fast to close compared with a bank, sometimes days.

Cons:

- You need existing revenue, so it is not a day-one option.

- The effective cost of capital can be high once you annualize the cap.

- It skims cash off the top every month, which can slow reinvestment during a ramp.

Best for: an operator already live who wants to add vehicles without a raise or a rigid loan. It pairs naturally with a revenue-share platform, since both your platform cost and financing cost scale with the same rider payments. Watch out for: stacking RBF on thin margins, where the revenue skim pushes vehicles below breakeven.

Option 5: Angel investors and venture capital

Equity financing means selling a share of the business for cash you never repay. Angels write smaller early checks; venture capital (VC) firms write larger ones and expect outsized growth.

How it works: investors buy equity, betting the company grows large enough that their stake is worth far more later. No repayments, but you have new owners.

Pros:

- Large sums with no repayment obligation, which can fund losses during an aggressive multi-market land grab.

- Strategic help, introductions, and credibility from the right investor.

- No collateral or personal guarantee.

Cons:

- Dilution and loss of control. You answer to a cap table and eventually a board.

- Growth expectations. VC is built for venture-scale outcomes, not steady single-city cash flow.

- Fundraising is slow and distracting, and most fleets never fit the profile.

Most fleets should not take VC

A single-city fleet that can reach breakeven on rides does not need venture capital and probably should not take it. Equity is the most expensive money you will ever raise if the business could have funded itself. Reserve it for genuine multi-market, venture-scale ambition.

Best for: operators pursuing rapid expansion across many markets who need capital faster than debt or cash flow can supply. Watch out for: raising equity to cover costs that a revenue-share model would have removed from your upfront number entirely.

How Levy's revenue-share model changes the capital math

Here is the part that changes every calculation above. Levy Fleets is $0 upfront and revenue-share: you pay when riders pay. That single fact removes an entire bucket from the money you raise.

On the Managed plan, Levy charges 20 percent of GMV under 100 active vehicles (and 15 percent of GMV at 100 to 249 active vehicles on annual or approved terms), with a 250 dollar per month platform minimum credited against your fees. GMV means gross rider payments before taxes, government fees, refunds, and tips. Your partner share defaults to 80 percent, the complement of that fee, and your actual payout is calculated on net revenue after Stripe processing (Levy's volume rate is 2.6 percent plus 0.20 dollars per transaction), with those processing costs shared proportionally. See the full pricing and plan detail for the exact structure.

For that revenue share you get the whole operating stack included, not gated behind tiers: nine software platforms (payments, SMS, support, credit and identity, push, marketing, fleet management, and ID verification), Levy-branded rider apps for iOS and Android (Levy Label), an operator dashboard, IoT connectivity, vehicle health tracking, city compliance, analytics, managed payments with disputes and collections, and 24/7 managed support. The included rider apps run under Levy Label, the Levy-branded app, which carries no setup fee. Publishing your own operator-branded app on both stores is a separate 2,750 dollar one-time white-label add-on, not part of the revenue share.

Re-read the three buckets from the start of this lesson:

| Cost bucket | Traditional path | With Levy revenue share |

|---|---|---|

| Operating stack (software, apps, payments, support) | Build or license and staff it, upfront | Included, paid as a percentage of revenue only when riders pay |

| Hardware | Buy or finance | Buy or finance (unchanged) |

| Working capital | Raise it | Raise it (unchanged) |

The operating stack drops out of the capital you have to raise. You are no longer financing software licenses, a payments integration, an identity and fraud stack, or a support team as upfront costs. Those become a share of revenue that only exists once the fleet is earning. The check you need collapses toward hardware plus working capital, and your only fixed floor is the 250 dollar per month minimum.

That compounds across every option above: a smaller loan, a smaller lease, a smaller RBF advance, a smaller (or unnecessary) equity raise, or a fleet you can now self-fund entirely. The best financing decision is often the raise you avoid because the operating costs became pay-as-you-earn. Cutting the capital you need usually beats optimizing the rate on a larger raise.

If you later build your own operations team and want to run in-house, the math shifts again: Software-Only is 14 dollars per vehicle per month at 100 to 249 active vehicles on an annual commitment, and Enterprise is custom at 250 or more vehicles. That is a deliberate later-stage choice, not a starting point.

Build your capital stack

Put it together in order. Each step narrows what you need and points you to the right instrument.

Size the fleet and find breakeven

Model your city, fleet size, and pricing in the Fleet Estimator and confirm how many rides per vehicle per day cover a vehicle's daily cost. You cannot size financing until you know the ramp.

Separate hardware from operating costs

Tag every cost as hardware, operating stack, or working capital. Only the first and third are yours to finance if you run on revenue share.

Choose the operating model to minimize upfront

Start on the $0-upfront revenue-share plan so the operating stack never hits your raise. Revisit Software-Only or Enterprise only after you have scale and in-house ops.

Match a financing source to the hardware

Pick the instrument that fits your stage: cash for a pilot, equipment financing to preserve cash, an SBA loan if you have history, or RBF once you are live and adding units.

Hold working capital for the ramp

Never spend your entire balance on hardware. Keep a cushion for charging, repairs, spare parts, rebalancing labor, and marketing until utilization stabilizes.

Which option fits your stage

Financing is stage-driven. The right instrument at 15 vehicles is the wrong one at 300.

A small starter fleet you are proving in one market. Self-funding or an equipment lease keeps you flexible, and the $0-upfront revenue-share plan means you finance only vehicles plus a working-capital cushion. Avoid rigid bank debt and equity here: utilization is unproven.

Frequently asked questions

Fund the fleet, not the platform

The operators who finance well raise the smallest amount they can and put every dollar behind vehicles that earn. Separate hardware from the operating stack, let the operating stack ride on revenue instead of your balance sheet, and match a financing instrument to your stage. Model the numbers first, then choose the money.

Scooter rental business profitability

The unit economics and assumptions behind fleet breakeven, so you know exactly how much capital your ramp needs to buy.

Ready to see how the revenue-share math plays out for your city and fleet size? Book a demo and we will walk through your capital stack line by line.